Sleep Number has gotten torched over the last six months - since January 2025, its stock price has dropped 49.5% to $7.74 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Sleep Number, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Sleep Number Will Underperform?

Even though the stock has become cheaper, we're cautious about Sleep Number. Here are three reasons why we avoid SNBR and a stock we'd rather own.

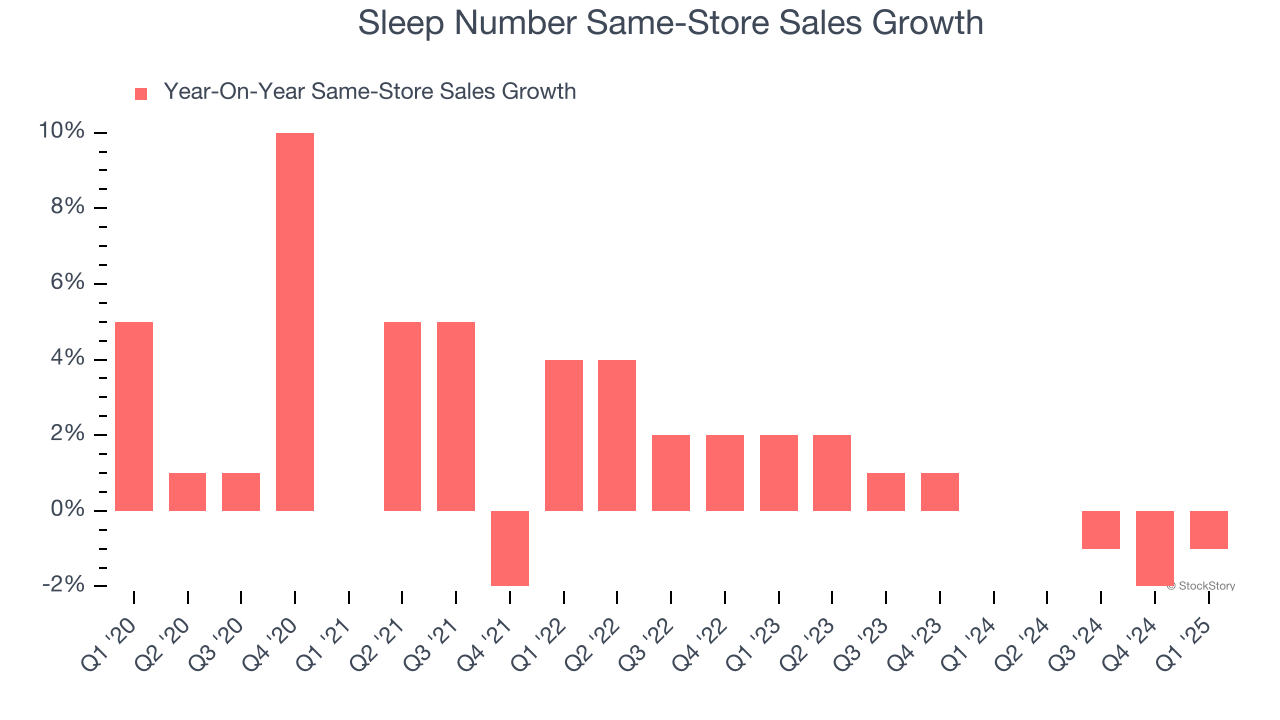

1. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Sleep Number’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Sleep Number’s revenue to drop by 4.6%, a decrease from This projection is underwhelming and indicates its products will see some demand headwinds.

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Sleep Number burned through $28.02 million of cash over the last year, and its $934.6 million of debt exceeds the $1.69 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Sleep Number’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Sleep Number until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Sleep Number doesn’t pass our quality test. Following the recent decline, the stock trades at 1.7× forward EV-to-EBITDA (or $7.74 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. Let us point you toward our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.