2021 was a year to forget for investors in the Gold Miners Index (GDX), with the ETF plunging more than 10% and massively underperforming the S&P-500's (SPY) 26% return. However, we have seen a slight change in character this year, with the GDX outperforming the major market averages and regaining its key moving averages. While relative strength has been fleeting in the past, this time could be different, given that the gold price (GLD) is also holding up well, and the miners as a group are the cheapest that they've been in years from a valuation standpoint. Let's look at three names that appear to be solid buy-the-dip candidates below:

(Source: TC2000.com)

While many investors prefer to use the GDX to gain leverage to the gold price, I see this as an inferior way to play the metal. This is because most gold producers are not that well-run, and about 20% of the sector is un-investable due to inferior operations or steadily declining margins. Instead, I believe the best course of action is hand-selecting the best producers, especially when many producers are returning significant capital to shareholders through both dividends and share buybacks.

When it comes to three elite miners that meet this criterion, I believe SSR Mining (SSRM), Newmont (NEM), and Nomad Royalty (NSR) are worthy selections. This is because all three companies have strong margins that range from 45% to 80%, they have solid management teams that have a track record of doing the right deals at the right time, and they all pay attractive dividend yields, ranging from 1.25% to 3.75%. Let's begin with SSR Mining:

SSR Mining is an intermediate gold producer, producing nearly 800,000 gold-equivalent ounces per year at all-in sustaining costs [AISC] near $1,000/oz. The company has three gold mines located in the United States, Canada, and Turkey and a silver mine in Argentina, giving it a diversified asset base. Prior to 2020, SSR Mining was a well-run miner, but it wasn't easy to justify owning the stock, given that its costs were well above the industry average.

However, with the company completing a merger of equals with Alacer Gold and adding the low-cost Copler operation in Turkey, SSR is a much better company, with AISC margins near 45%. Meanwhile, since Alacer's CEO took over at the helm of SSR Mining, the company has seen significant exploration success and has begun a generous capital returns program, buying back over 4% of its float this year and announcing a dividend. Based on a current price of $16.50, its dividend comes in at 1.25%, and I believe there's room to increase this dividend over the next 18 months to more than $0.25 per share annualized.

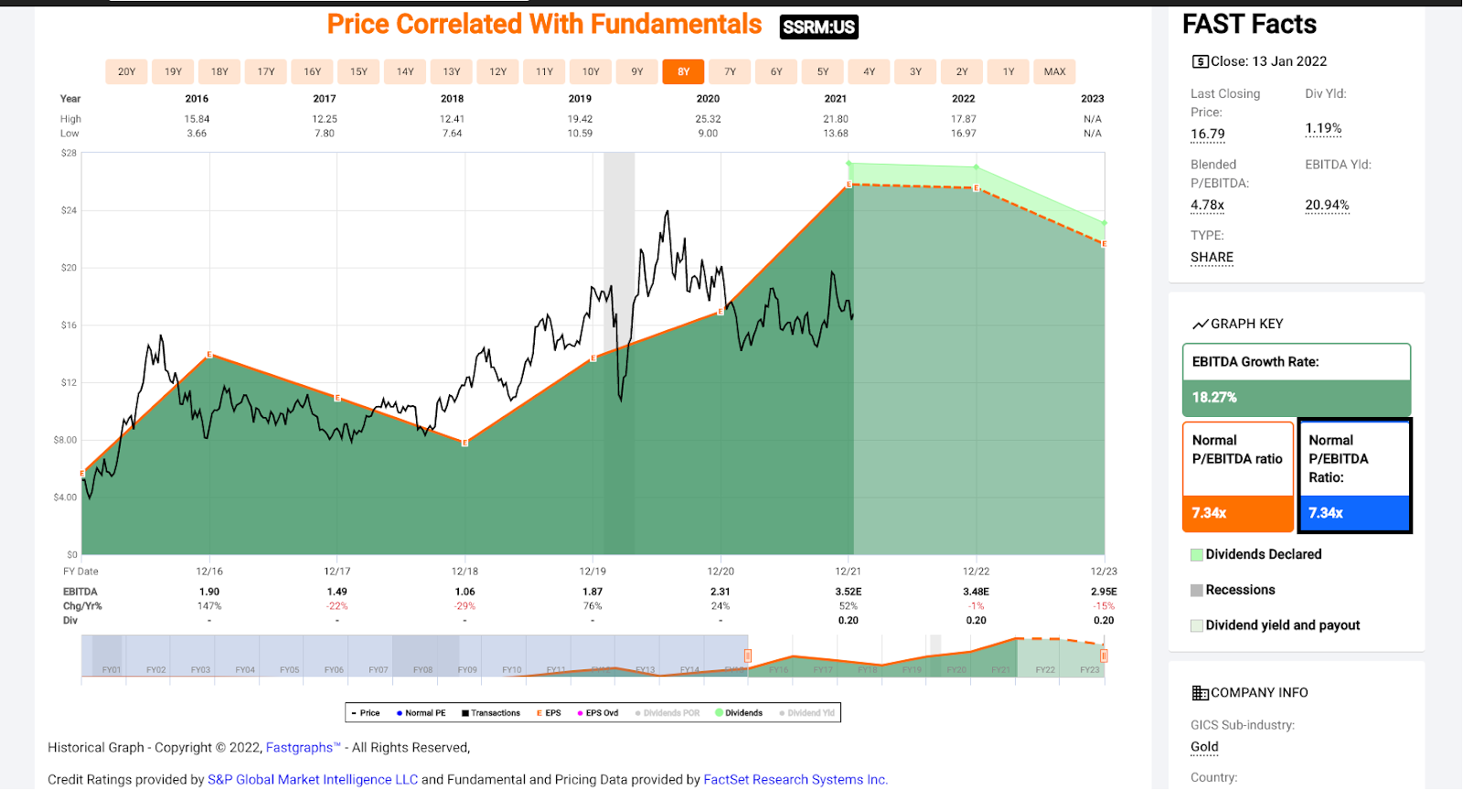

(Source: FASTGraphs.com)

Despite an improved long-term outlook with the addition of the low-cost Copler Mine in Turkey, and growth opportunities adjacent to Copler (Ardich), SSR Mining trades at a very reasonable valuation, which is shown above. This is because it currently trades at ~4.7x FY2022 EBITDA estimates vs. a historical multiple of 7.3x estimates. Even if we use a more conservative EBITDA multiple of 6.5 to account for the inflationary pressures, which are a minor headwind to margins sector-wide, I see a fair value for SSR Mining of $22.00 per share. After applying a 30% discount to fair value to bake in a margin of safety, I would view any pullbacks below $15.40 as low-risk buying opportunities.

Moving to Newmont, the company shouldn't need any introduction for those familiar with the sector, given that it's the world's largest gold producer, with more than 13 operations across multiple continents. As it stands, more than 55% of the company's production comes from Tier-1 ranked jurisdictions, which include Canada, Australia, and the United States, based on the Fraser Institute Survey.

Despite a massive production profile and an enviable development pipeline, Newmont's stock has come under pressure due to inflationary pressures related to fuel, consumables, and labor, as well as COVID-19 related headwinds. This has dented margins, with cost estimates revised higher to account for these headwinds. It's important to note that this is a sector-wide issue, and it is not company-specific. Meanwhile, given NEM's strong balance sheet with minimal net debt, NEM can invest aggressively in technology, innovation, and new higher-margin projects to offset these cost pressures.

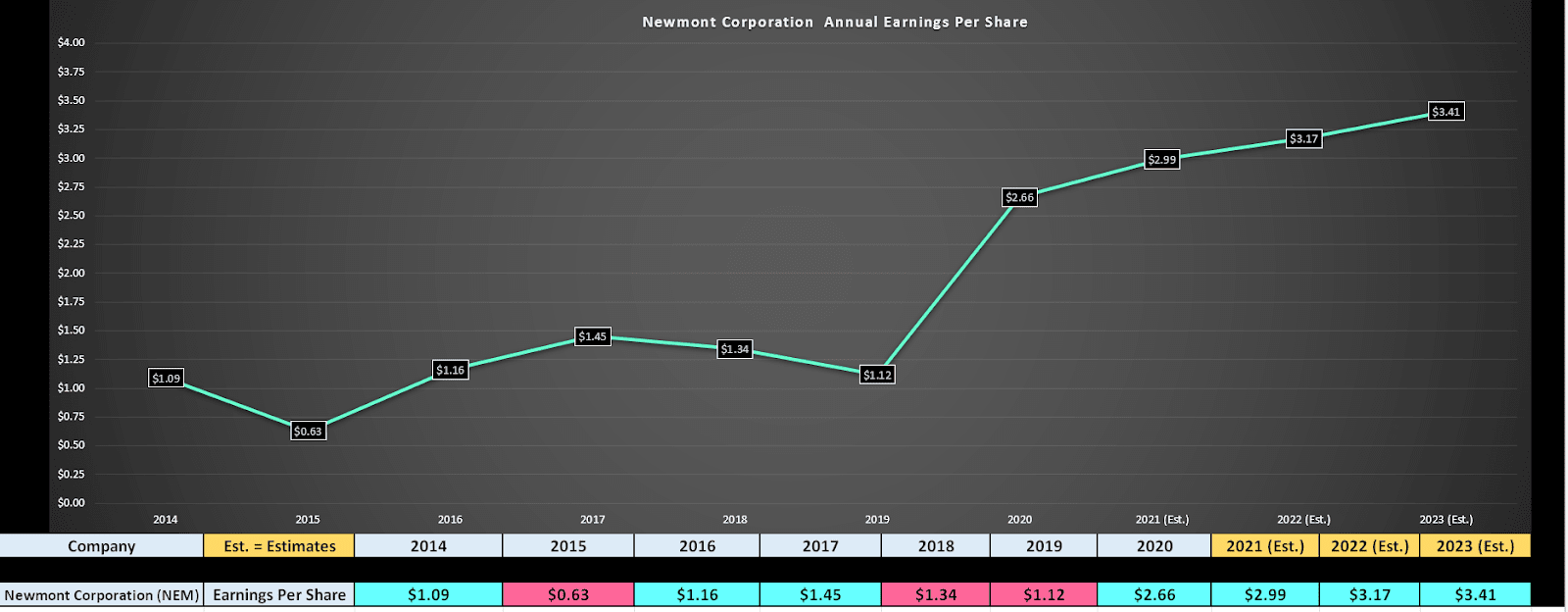

This is great news for the company relative to its peers because it means that while costs may rise short-term in FY2022 and FY2023, NEM should be able to claw most of the margin pressure. It's also worth noting that while NEM's costs are rising, they're still expected to come in at $1,030/oz in FY2022 and drop to $930/oz in FY2024/FY2025. These are still very attractive margins when we have a gold price that has traded between $1,700/oz to $1,950/oz over the past 18 months. Hence, NEM is still a very profitable company, evidenced by its earnings trend below.

(Source: YCharts.com, Author's Chart)

As noted, given the disruptions to NEM's operations, the company has seen a decline in its share price from its all-time high near $75.00 to $60.00 per share. At this level, the stock trades at just 19x FY2022 earnings estimates, which is a very reasonable valuation for a company with 30% operating margins. The bonus to owning NEM is that the stock pays an annualized dividend yield of $2.20, and I believe there's upside to $2.40 next year. So, at a current share price of $60.00, investors are collecting a 4% yield on cost, assuming a slight dividend raise. With what I believe to be a fair value of closer to $70.00 per share, I would view any pullbacks below $55.50 as low-risk buying opportunities.

The last name on the list is Nomad Royalty, a much smaller company than NEM ($47BB) and SSR Mining ($3.5BB), with a market cap of just $440MM. However, Nomad has a unique business model, acquiring royalties and streams on gold, silver, and copper projects in exchange for an upfront payment to help these companies strengthen their balance sheet or fund expansion/construction of their projects. To date, the company has 14 royalties and streams across multiple continents and is expected to generate more than $60MM in revenue in FY2023.

At more than 7x FY2023 revenue estimates, some investors might believe that this is an expensive valuation. However, this is actually a very reasonable valuation. This is because Nomad has 80% plus margins because it is not mining or spending any capex, but instead collecting payments from its royalty/streaming assets. Typically, royalty/streamers trade at more than 12x sales, with the largest royalty/streamers like Franco Nevada trading at more than 18x forward sales. Hence, at 7x FY2023 estimates, the stock is attractively relative to its peer group.

(Source: SEDI Insider Filings)

While not a massive number dollar amount, insiders seem to agree that the stock is undervalued, purchasing more than $100,000 worth of shares over the past two months. So, why own the stock?

Unlike other royalty/streamers that have low single-digit compound annual growth rates for their attributable production (ounces attributable to them from producing assets that they sell for revenue), NSR has one of the highest growth rates sector-wide. This is based on the fact that it expects to grow attributable production from 20,000 gold-equivalent ounces [GEOs] per annum in FY2022 to 50,000 GEOs per annum in 2025 and 60,000 GEOs per annum in 2029.

This growth profile dwarfs that of the company's peers, making NSR a high-growth name at a reasonable price. Finally, while producers are struggling to hold the line on margins due to inflationary pressures, royalty/streamers like NSR are not having this issue. This makes it a superior way to play the sector, and I see the stock as a Strong Buy on dips, with a fair value above $10.50 per share.

After a year of underperformance, it's understandable that many don't want to invest in the gold sector, especially when gold has been proclaimed to be dead. However, it's exactly when sentiment gets this bad that it's the best time to invest in the precious metals sector, given that the sector cycles from one extreme to another. In August 2020, when investors were calling for $3,000/oz gold and $60/oz silver, it was time to dump miners and stay out. At $1,800/oz and $22/oz silver, we now have little optimism left, and the stocks are hard to give away. Given this improved sentiment profile, I see SSRM, NSR, and NEM as great buy-the-dip candidates to play a 2022 rebound in the sector.

Disclosure: I am long GLD, NEM, NSR

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

NEM shares were trading at $61.17 per share on Friday afternoon, down $0.15 (-0.24%). Year-to-date, NEM has declined -1.37%, versus a -2.58% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Miners to Pick Up Now With 7% Inflation appeared first on StockNews.com